As a member of the baby boomer generation, you have spent your career building a successful business. Now approaching retirement age, you may consider selling your business to the next generation of Gen X looking to purchase their first business. This can be a complex and emotional process. But with proper planning and preparation, you can ensure a smooth transition and maximize the value of your business.

This is not a problem that you're confronting alone. In fact, you're in good company.

What is a "Baby Boomer"?

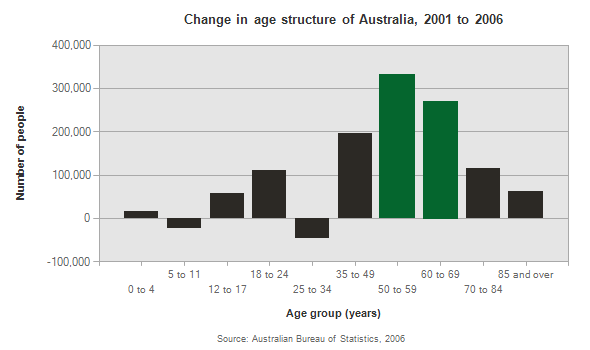

The Australian Bureau of Statistics estimate that more than 100 thousand baby boomers in Australian will be looking to sell their business between 2023 - 2026.

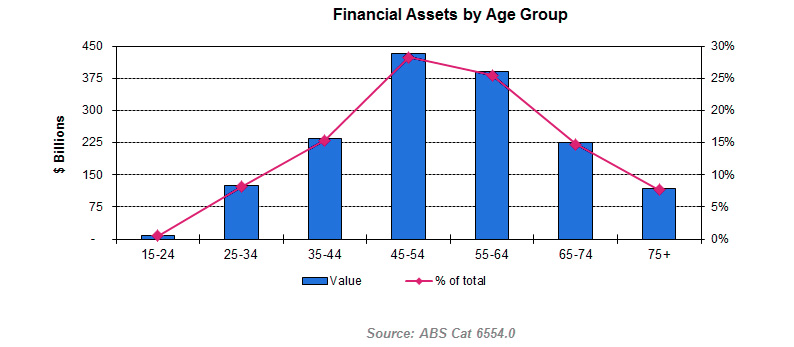

The financial assets owned by the baby boomers (including businesses) represents an enormous segment of overall wealth in Australia.

The baby boomer generation is defined as those born between 1946 and 1964. This generation is currently going through a retirement wave. According to a recent survey by the Australian Bureau of Statistics, nearly half of all baby boomers plan to retire within 2022 - 2026. If you are among this group and own a business, you may be wondering how to sell your business to the next generation.

Selling a business to the next generation has several distinct advantages over selling to a third party:

- You can pass on your legacy to someone you trust and who shares your values.

- It can provide a smooth transition for both the business and its employees, as the new owner is likely familiar with the company's operations and culture.

- It can often result in a higher sale price, as the buyer is more comfortable with the terms of the sale and may be more willing to pay a premium to keep the business in the family.

Preparing your business for sale to the next generation

Before you can sell your business to the next generation, you need to prepare it for sale. The constant day-to-day hustle of running a business may leave little time for preparation. So allocate specific time towards organising and preparing the business for sale.

Here are some steps you should take:

- Understand the value of your business

You will need to have a clear understanding of the value of your business before you can set a realistic price for your business. There are several methods you can use to determine the value of your business, such as a discounted cash flow analysis or a multiple of earnings method (EBITDA). A business broker or financial advisor such as Lloyds Corporate Brokers can help you determine the value of your business. Lloyds use a variety of tools for valuing and benchmarking businesses.

- Update financial records and documents

Potential buyers (even if they are relatives) will require up-to-date financial records and documents, including profit and loss statements, balance sheets, and tax returns. Make sure these documents are organized and accurate.

- Marketing your business to potential buyers

Once you have prepared your business for sale, you will need to let potential buyers know it is available. This can be done through a variety of methods, such as advertising in industry publications, working with a business broker such as Lloyds, or approaching potential buyers within your family or personal network. Lloyds Brokers have a wide network of national and international buyers who are ready to purchase businesses.

Finding the "right fit" to buy your business

You walk into a shoe store and see thousands of shoes for purchase. But only a handful of them will be the "right fit" for you " accommodating your aesthetic preference, desired function and size of foot. Buyers for a business are just like shoes. There are many potential buyers, but usually only 1 or 2 are the "right fit" to buy your business " in terms of culture, values and vision.

Once you have prepared your business for sale, the next step is to start the journey to find this right buyer that fits your business. Here are some steps to consider:

- Identify potential buyers within your network

Your network of colleagues, employees, and customers may include individuals who are interested in buying your business and share your values and vision. Consider reaching out to these individuals and see if they are interested in learning more.

- Work with a business broker or financial advisor

A business broker or financial advisor can help you find potential buyers and negotiate the sale of your business. They can also help you set a fair price and establish terms of sale that both parties agree on. Although these professionals will charge a fee, the fee is usually more than fully offset by the higher sale price or better terms negotiated on your behalf. Lloyds bring many advantages to the sale process - experience, a database of buyers and the ability to maximise the sale price. Read more about the Lloyds advantage here.

- Consider alternative options such as employee stock ownership plans (ESOPs)

If you are unable to find a buyer within your network and you also do not want to work with a broker, you may want to consider alternative options such as selling to a third party or implementing an employee stock ownership plan (ESOP). An ESOP allows your employees to buy shares in the company and eventually take ownership of the business.

Negotiating the sale of your business

- Set a fair price for your business

The price of your business should be based on its value, as determined by a neutral third party (an accountant, financial consultant or business broker). It is important to be realistic about the value of your business and not to allow emotions to influence the price you set.

- Determine the terms of the sale

In addition to the price of the business, just as critically important are the terms of the sale, including the payment schedule, any financing arrangements, and any contingencies.

- Draft and review the purchase agreement

Once you have agreed on the price and terms of the sale, you will need a purchase agreement to be drafted by a solicitor. Review this agreement carefully with your solicitor to ensure that it protects your interests and accurately reflects the terms of the sale.

Transitioning the business to the new owner

Once the sale of your business is finalized, the next step is to transition the business to the new owner. Here are some things to consider:

- Provide training and support to the new owner

The success of the transition will depend in part on the new owner's ability to effectively run the business. Consider how often and on what terms you will be available to the new owner to provide training and support.

- Maintain confidentiality during the transition period

Maintaining confidentiality during the transition period will help to avoid disruptions to the business. This may include restricting access to certain information or not discussing the sale with employees or customers.

- Deal with emotional challenges of letting go of your business

Selling a business that you have built from the ground up can be an emotional process. After all, a significant portion of your life has been dedicated to something that is now being handed over to the ownership and control of another person. It is not uncommon for the transition to invoke strong emotions of despair, disorientation, and discomfort. Rather than ignore these emotions or pretend that they don't matter, it is important to recognize and deal with them in a healthy way. Seeking support from friends, family and a therapist are highly recommended.

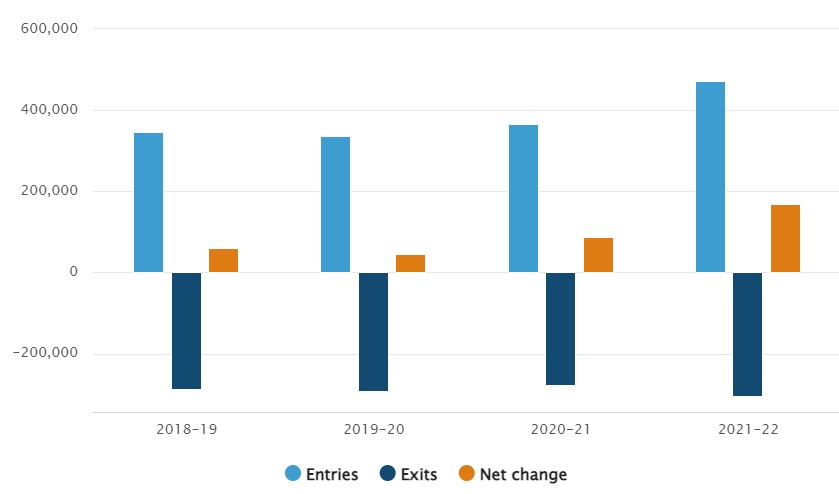

According to the Australian Bureau of Statistics, between 2018 - 2022, Australia experienced an average annual turnover of business entry and entries of 12% - 19%. Many of these businesses were sold using a broker.

Australian business entries and exists (2018 - 2022)

Source: Australian Bureau of Statistics

Selling your business to the next generation can be a complex and emotional process. With proper planning and preparation, you'll ensure a smoother transition and maximize the value of your business. Key steps to consider include:

- preparing your business for sale

- finding the right buyer (the "right fit" for your business)

- negotiating the sale

- transitioning the business to the new owner

- addressing your emotional needs

By following these steps, you can retire with confidence knowing that you have passed on your legacy to someone you trust.

Geoffrey

Director Lloyds Corporate Advisory - Mergers & Acquisition Specialist

Geoffrey

Director Lloyds Corporate Advisory - Mergers & Acquisition Specialist

Dianne

Director Research, Mergers & Acquisition Specialist

Dianne

Director Research, Mergers & Acquisition Specialist

Paul

Mergers & Acquisition Specialist

Paul

Mergers & Acquisition Specialist

Wayne

Lloyds Corporate Partner - Agricultural, Regional Manufacturing Specialist

Wayne

Lloyds Corporate Partner - Agricultural, Regional Manufacturing Specialist